64 / 76

64 / 76

64

// PUBLIC GAMING INTERNATIONAL // July/August 2016

banking fees across all of their card sales

and calculate a blended rate for accept-

ing credit and debit cards.

Interchange:

Rather than go into the complexity

and details of all of these fees, we’ll focus

on Interchange, the most prominent of

the fees that best illustrates the concept

of a blended rate and the impact of the

fixed and variable components.

Interchange can be very complicat-

ed—there are many interchange catego-

ries established by each of the payment

networks across their range of products

(credit, debit, gold, platinum, corporate,

etc.) as well as the different categories of merchant. For this

exercise, we’ll use the most common Visa interchange categories

we expect to see for retail lottery transactions.

For “Regulated Visa Check Cards” (Visa Debit Cards issued

by banks with more than $10B in assets), the rate of 0.05%

+ $0.21 is particularly illustrative of the challenges that exist

for small-dollar transactions. On a $1 transaction, interchange

alone would result in a blended rate of 22%. That is simply not

sustainable in our business; however, as you move to $10 or $25

transactions, the blended rate drops quickly to a much more

manageable level of 2.2% and 0.9%, respectively.

The Credit rate, “CPS/Retail 2” at $0.05 + 1.43%, has much

less of an impact on small-dollar sales, with a blended rate for

a $1 transaction down to 6.4%—still problematic for a $1 sale,

but higher amounts also bring the credit interchange rate to a

more manageable level.

To fully understand the impact of these fees,

lotteries should think differently about

Clerk-Activated vs. Self-Service sales.

Clerk-activated lottery sales are likely part of a larger shopping

basket, for which the retailer will have already incurred all of the

fixed banking fees for the non-lottery parts of the transaction. If a

consumer adds lottery to an existing transaction for the purchase of

bread, milk, and cereal, the retailer’s banking fees only increase by the

variable cost components. In the debit card example shown above,

the $0.21 is already covered in the non-lottery purchase, so the in-

cremental interchange on the lottery ticket is only 0.05%. We see the

same effect on the credit interchange—only the 1.43% applies.

Therefore, for clerk-activated lottery transactions, a business

case can be made for the retailer to incur the banking fees, since

the lottery products are part of a larger transaction, and they’re

already paying the fixed fee components for the non-lottery

items in the basket.

However, self-service lottery sales must bear the full

economics of the banking fees.

Unfortunately, self-service lottery sales stand alone and in-

cur the full set of banking fees, fixed and variable; however, it

is expected that enabling card purchases will drive incremental

sales. After a review with Visa and leading merchant acquirer

Vantiv, we looked at other markets, including fast-food res-

taurant, vending machines, etc.—lottery could see as much as

an 18% sales lift on card-enabled self-service machines. While

banking fees could consume much of a retailer’s commission if

the retailer pays them, lottery profits on these incremental sales

should be at least five times the banking fees—a solid return on

the “investment.” Therefore, lotteries should consider bearing

the cost of the banking fees for the self-service environment.

To illustrate the business case, the following is a simple ex-

ample of the self-service machine economics.

Assumptions:

• Weekly sales per unit: $3,500.

• Incremental sales: 18%.

• Cannibalization of existing cash sales: 20%.

– NOTE: the reality is that some existing cash transactions

will convert to card sales, for which banking fees

will incur.

• Average card transaction: $15 assumption.

– NOTE: we have a few data points in the market that

give us confidence this is a realistic benchmark, perhaps

even conservative.

• Card type(s) accepted: debit cards only.

• Blended rate for all banking fees: 2.15%.

• Lottery profit: 30%.

• Retailer commission: 6%.

EXHIBIT

1

:

When lottery is part of a larger shopping basket, only the variable fees apply when looking at the marginal

cost of accepting credit transactions

Clerk-Activated Transactions:

Incremental cost of lottery to an existing shopping basket

DEBIT Card:

$0.21 + 0.05%

The Rate:

Variable: ........................0.05%

Fixed:.............................$0.21

The Impact:

$1 purchase: ..................22.0%...............0.05%

$10 purchase:................2.2%.................0.05%

$25 purchase:................0.9% ................0.05%

CREDIT Card:

$0.05 + 1.43%

The Rate:

Variable: ........................1.43%

Fixed:.............................$0.05

The Impact:

$1 purchase: ..................6.4%.................1.43%

$10 purchase:................1.9% .................1.43%

$25 purchase:................1.6% .................1.43%

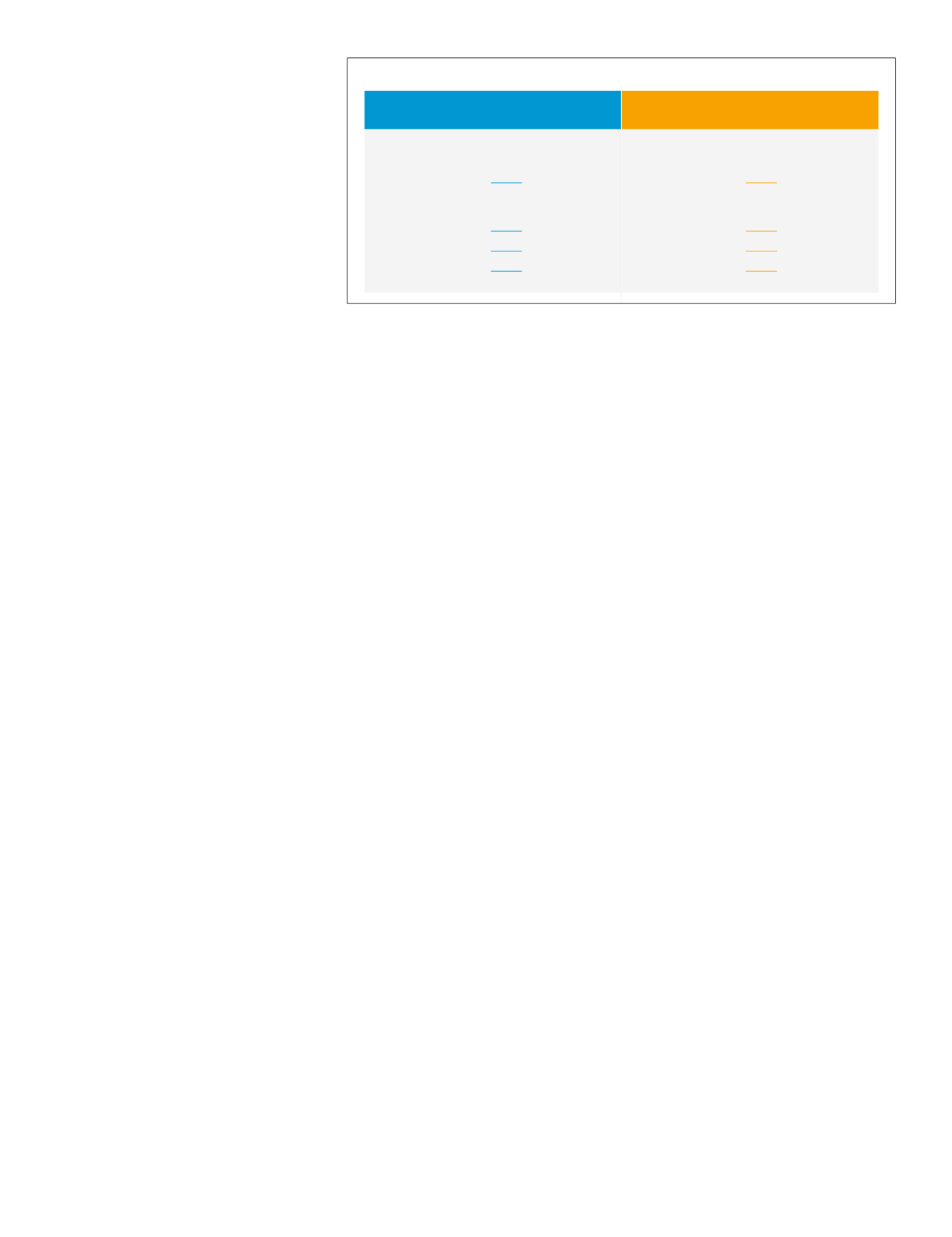

Debit card only

Weekly Sales:................................................$3,500

(self-service per unit)

Sales Lift:.......................................................18%

Canniba ization of Cash:............................. 20%

Average Ticket:............................................$15

Banking Fees: ............................................... 2.15%

Lottery Profit................................................30%

Retailer Commission ...................................6%

Incremental Sales

Profit / Commission

Banking Fees

Net

$630

$630

$189

$38

($29)

($29)

$160

$9

EXHIBIT

2

:

Hypothetical comparison of Return on Investment for lottery and retailer if banking fees are included

Self-Service:

Should lottery bear cost of banking fees?

LOTTERY

RETAILER

Self-Services Assumptions:

Exhibit 2: When lottery is part of a larger shopping basket, only the variable fees apply

when looking at the marginal cost of accepting credit transactions.