63 / 76

63 / 76

July/August 2016 // PUBLIC GAMING INTERNATIONAL //

63

A

s lottery has historically been a cash-only industry,

we are early on in the learning curve for accepting

other forms of payment. With “cashless,” a great op-

portunity awaits us—to embrace the next genera-

tion of lottery players and drive incremental sales and profits to

good causes.

Cashless includes traditional credit, debit, and gift cards, as

well as newer methods, such as PayPal or ApplePay and oth-

er mobile payment models. These are all well supported by

the many technical solutions available in the market, but the

greatest challenge for lotteries is to understand and accept the

economics related to cashless—i.e., the benefits and costs of

the investment in expanding the payment options available to

lottery players.

Cashless is about customer service—for players

and retailers.

Consumers prefer choice and respond much better when you

bring your products to them, via their favored medium and

channel, and support their ideal way

of paying. While cash will never go

away completely, it is no longer pre-

ferred, particularly with the younger

generation, who shop with a card or

their mobile device and often don’t

even carry cash.

Your retailers and players, current

and prospective, will be more recep-

tive to a cashless lottery, its brand, and

its products.

Ultimately, this is about optimizing prof-

its for the lottery and its retailer partners.

While there are costs related to cashless, they are an

investment in the future growth of lottery sales.

It is important to view cashless as an “investment” as we re-

view its related costs—the banking fees—and who should bear

these costs—the lottery or the retailer.

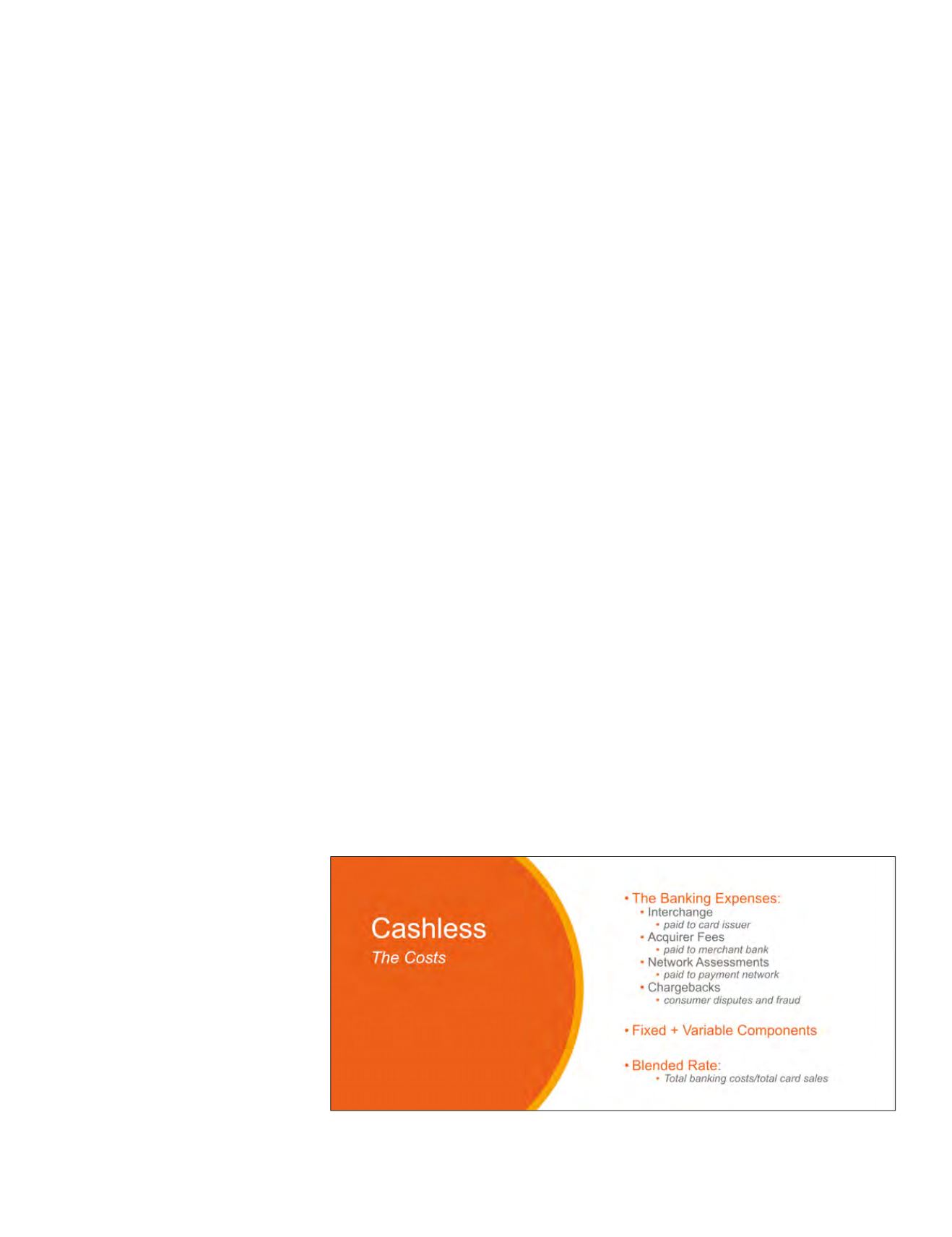

Let’s begin with an explanation of the components of bank-

ing fees related to accepting credit and debit cards. There are

quite a few layers to this, each with fixed and/or variable cost

components, including:

•

Interchange

that is paid to the issuer of the card.

•

Acquirer Fees

for the merchant banking partner who

processes the transaction.

•

Network Assessments

owed to the payment network

(e.g., Visa or MasterCard).

•

Chargebacks

related to customer disputes or fraud.

Most retailers don’t review this at the individual transaction

and fee component level. Rather, they typically review the total

Choice for the Modern Consumer:

Lottery & Cashless Payments

By Andrew Crowe, Vice President, Interactive Payments, IGT

Exhibit 1: An example of the banking fees involved in accepting credit and debit cards.