WLA BLOG: Lotteries and sports betting operators emerge largely unscathed from pandemic

After a tumultuous three years, the world's state-regulated lottery and sports betting operators have emerged largely intact from the depredations of the COVID-19 pandemic. In FY 2022, revenues increased across the sector by approximately 10% over the previous corresponding period, with gains made on the return to retail and strong one-off sporting events in particular.

- World progressively relaxes COVID-19 restrictions in a return to pre-pandemic normality.

- COVID-19 still circulating at elevated levels, as the world transitions to endemicity.

- Pandemic costs begin to emerge with global life expectancy decreasing for the first time since the 1960s and economic losses estimated as at least USD 2.6 trillion in the US alone.

- IMF estimates global real GDP growth of 3.4% for 2022 with inflation rising to 8.8%, giving rise to difficult macroeconomic conditions into Q1 2023.

- Lotteries build on 2021 recovery from the pandemic with H2GC estimating 10.1% growth in lottery and sports betting revenues for 2022.

- Return to retail, one-off sporting events, and strong growth in the digital channel power lottery and sports betting bounce back.

- H2GC now projecting total global gross win (land-based plus interactive) to surpass pre-pandemic levels by end 2023.

In our continuing coverage of the COVID-19 pandemic and its impact on the global lottery and sports betting industry, we report on the global transition to living with the virus in a new normal and the concomitant response of the global lottery and sports betting industry. COVID-19 is becoming an endemic disease that will likely always be with us; however, thanks to the advent of efficacious vaccines, the link between cases and deaths in highly-vaccinated societies has – per The Lancet medical journal – been weakened, if not quite broken. Indeed, with the development of effective vaccines on the one hand, and high levels of vaccine-induced or hybrid population immunity on the other, The Lancet hopes that the severity of COVID-19 (after accounting for patient age and underlying conditions) is becoming closer to that of seasonal influenza.

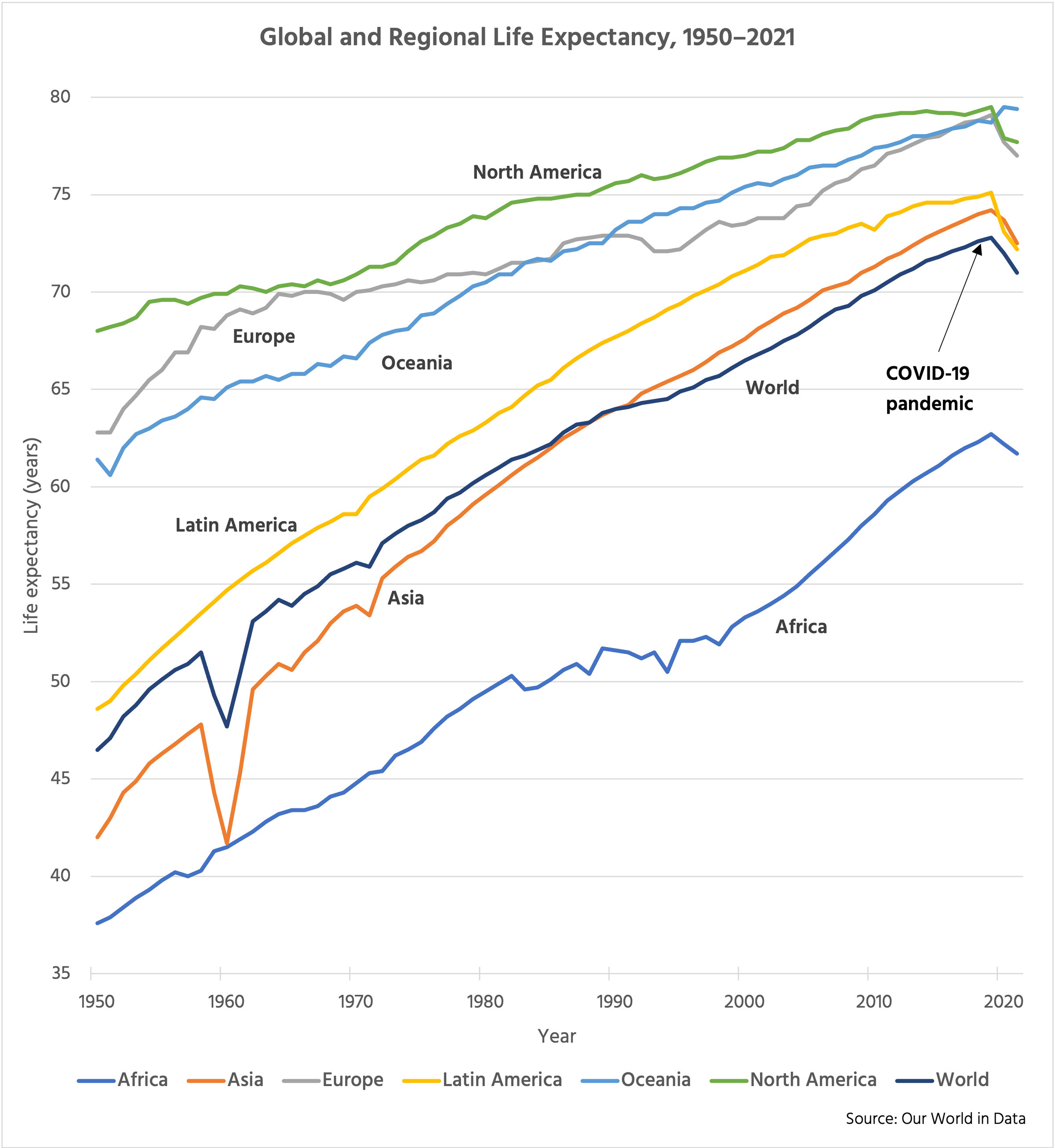

Nonetheless, the damage wrought by the pandemic to humanity has been severe. For the first time since the 1960s, global life expectancy has fallen, by more than a year; outside the US, the decrease in life expectancy has been largely pandemic-related. See Figure 1. According to the journal Nature, more than ten million children have lost a parent or carer to the pandemic. And, the economic toll of the global health crisis has been immense, with the cost of COVID-19 in the US alone being estimated variously at anything from USD 2.6 trillion to USD 3.7 trillion at a minimum, according to studies from Harvard University.

Figure 1. Decline in Life Expectancy since the Onset of the COVID-19 Pandemic.

Three years into the pandemic, the lottery and sports betting sector has emerged relatively unscathed from the global tumult caused by COVID-19. Despite lockdowns that severely impacted retail footfall and an absence of sporting fixtures that afflicted sports betting opportunities, both at the beginning of the pandemic, the sector rebounded in 2021, moving aggressively to online, optimizing retail sales channels otherwise, and innovating game content through new product launches and via the additions of extras and sundries to existing brands. In 2022, with the worst of the pandemic apparently in the rear view mirror, the industry has gone from strength to strength. Indeed, for lottery and sports betting operators reported upon in this bulletin, sales have increased by approximately 8.6% year-on-year, as summarized for selected entities in Table 1.

| Domicile | Entity | FY 2022 Sales (USD) (bn) | FY 2021 Sales (USD) (bn) | Delta (%) |

|---|---|---|---|---|

| AU | The Lottery Corporation | 1.4 | 1.3 | 7.7 |

| BR | CAIXA | 4.3 | 3.4 | 25.6 |

| CA | OLG | 3.7 | 3.5 | 6.7 |

| CN | China Sports | 42.9 | 35.8 | 19.7 |

| CN | China Welfare | 23.0 | 22.1 | 4.1 |

| DE | Deutscher Lotto- und Totoblock (DLTB) | 9.4 | 9.3 | 0.9 |

| FR | FDJ | 24.4 | 22.4 | 8.7 |

| GR | OPAP | 2.3 | 1.8 | 26.0 |

| HK, CN | HKJC | 37.3 | 36.0 | 3.6 |

| MA | MDJS | 0.5 | 0.4 | 6.9 |

| SE | Svenska Spel | 0.9 | 0.9 | -1.3 |

| SG | Singapore Pools | 7.5 | 5.3 | 42.1 |

| UK | Camelot | 11.1 | 11.5 | -3.4 |

| US | California Lottery | 8.9 | 8.4 | 5.2 |

| US | Georgia Lottery | 5.8 | 6.0 | -4.0 |

| US | Texas Lottery | 8.3 | 8.1 | 2.3 |

| ZA | Ithuba | 0.5 | 0.4 | 9.8 |

| Total | 192.2 | 176.9 | 8.6 |

Table 1. Year-on-year results for selected lotteries and sports betting operators reporting in this bulletin.

Key drivers leading to the positive results for the sector include:

- The easing of pandemic restrictions worldwide, which has resulted in increased footfall across retail globally, which has in turn driven retail network sales and a recovery in land-based gaming more generally.

- The one-off events UEFA 2020 European Championships (held in 2021) and the 2022 FIFA World Cup have led to big one-off increases in sports betting, especially in China.

- The continued growth of the digital channel globally, driven by the response to the pandemic on the one hand, by the development of immersive betting applications and the increasing convenience of gaming on mobile devices, together with the ongoing liberalization of sports betting worldwide, most notably in the US.

In consequence, for the financial year 21/22 or calendar year 2022, most state-regulated lotteries and sports betting operators have enjoyed substantial growth, sometimes to record levels of lottery sales. In jurisdictions where sales have declined year-on-year, this has been a consequence of local conditions rather than any general industry downturn. Further, modulo some exceptions, the inflationary pressures and difficult macroeconomic conditions witnessed towards the end of 2022 have not yet impacted the industry significantly.

In the sequel, we take a closer look at the above for some of the world’s major lottery and sports betting entities (and a smattering of smaller operators) across Africa, Asia Pacific, Europe, and Latin America, setting their operations and pandemic response in the context of current local conditions. For North America, where the state-based system gives rise to many operators, we consider several individual state-regulated lotteries, and make some comments on the market as a whole, highlighting sports betting operations in particular.

Africa

Of Africa's 54 nations, it has been South Africa and Morocco that have been hardest hit by the COVID-19 pandemic. Of the continent’s 12.8 million confirmed cases, fully 31.7% or 4.1 million cases have been in South Africa, with another 1.2 million (9.4%) in Morocco. South Africa in particular endured some of the most stringent pandemic measures imposed in the continent, including sustained lockdowns where the purchase of non-essential items, including lottery tickets, was prohibited. After a difficult two years, COVID-19 restrictions were lifted in South Africa in June 2022; Morocco’s state of health emergency was officially rescinded this past February. In 2023, the World Health Organization (WHO) reports that Africa is embarking on the fourth year of the pandemic with the hope of moving past its emergency response mode, thanks to broadened vaccination efforts – 29% of the population’s continent is vaccinated as of January 2023, up from just 7% a year earlier – and better treatment regimes, which together are helping to decouple disease incidence from serious adverse outcomes.

Asia Pacific

Despite being at the epicenter of the COVID-19 pandemic, Asia Pacific has been more successful than many other parts of the world in managing its response to the global health crisis, perhaps thanks to previous experiences with the SARS epidemic of 2002-2003 and the outbreak of MERS in Korea in 2015; Singapore in particular has had a model response, with very high (96%) vaccination rates and a case fatality rate of just 0.08%. India, with more than 44 million confirmed cases, was the country most impacted by the pandemic until November–December 2022, when China relaxed its ‘zero-COVID’ policy; at the time of writing, China has now seen more than 100 million confirmed cases of COVID-19. Australia, like several other countries in the Asia Pacific region, has steered a middle course, initially adopting a ‘zero-COVID’ policy in the absence of vaccines before pivoting to a ‘living with COVID’ policy in October 2021 after 70% of the population was vaccinated; the Australian government emergency response to COVID-19 ended in September 2022.

Europe

As of November 2022, Europe was the region most affected by the COVID-19 pandemic in the world, with France, Germany, and the United Kingdom among the worse-affected countries in terms of total case counts; collectively, the countries of Europe have accounted for nearly 36.8% of cases globally. (For contrast, Europe accounts for approximately 9.4% of the world’s population.) Nonetheless, as elsewhere in the world, most European countries progressively rolled back COVID-19 restrictions following aggressive vaccination campaigns, accepting the endemicity of COVID-19 in a return to the ‘new normal’. Thus, all restrictions in the United Kingdom were lifted in February and March 2022; Greece relaxed restrictions from May 2022; and France transitioned to the endemic phase of COVID-19 by August 2022, having lifted restrictions progressively from February 2022. In Germany, leading virologist Christian Drosten, head of virology at Charité University Hospital in Berlin, felt able by December 2022 to assert that the COVID-19 pandemic was largely over; according to calculations by the Munich Ifo Institute, the pandemic has reduced Germany's economic output by at least EUR 330 billion since March 2020. An outlier among the countries of Europe, Sweden pursued a ‘laissez-faire’ or ‘live and let live’ approach to managing COVID-19, with the country having never formally locked down at any point during the pandemic.

Latin America

The COVID-19 pandemic has been particularly bad in Latin America. Brazil remains one of the world’s most heavily impacted nations, behind only the United States, China, and India. In particular, it has been the country worst impacted in Latin America; of Latin America’s 68.3 million confirmed cases of COVID-19, fully 54.6% (37.3 million) have been in Brazil alone. Today, approximately 85% of Brazilians are at least partially vaccinated, and most states in Brazil are no longer enforcing COVID-19 restrictive measures.

North America

North America’s COVID-19 response has been dominated by the US, which has continued to have among the world’s poorest pandemic outcomes to date, at more than 102 million confirmed cases and 1.2 million fatalities. Management of the pandemic in the US has been driven in part by a highly politicized and polarized response to the global health crisis. Canada has fared somewhat better in its pandemic management, owing to a more coherent response built on the back of a broad-based vaccination program. Following a January 2022 COVID-19 wave (Omicron), restrictions across Canada were lifted by mid-2022, as case loads began to decline across the country, while in the US, the national emergency occasioned by COVID-19 was terminated on 10 April 2023. This national emergency was separate from the public health emergency associated with the COVID-19 pandemic, which will remain in force until 11 May 2023.

Outlook

The COVID-19 pandemic has been unprecedented in living memory, a sui generis event that has caused vast disruption – often with adverse consequences – globally, regionally, nationally, and individually, to businesses, governments, and members of the public alike. The good news is that – as The Lancet medical journal reports – at least in highly vaccinated countries the link between incidence of COVID-19 and severe outcomes has been weakened, if not quite broken. The upshot is that COVID-19 is becoming an endemic disease that will most likely always be with us. While endemic does not necessarily mean mild, The Lancet is hopeful that with high levels of population immunity, the severity of COVID-19 will become closer to that of seasonal influenza, after accounting for patient age and underlying conditions.

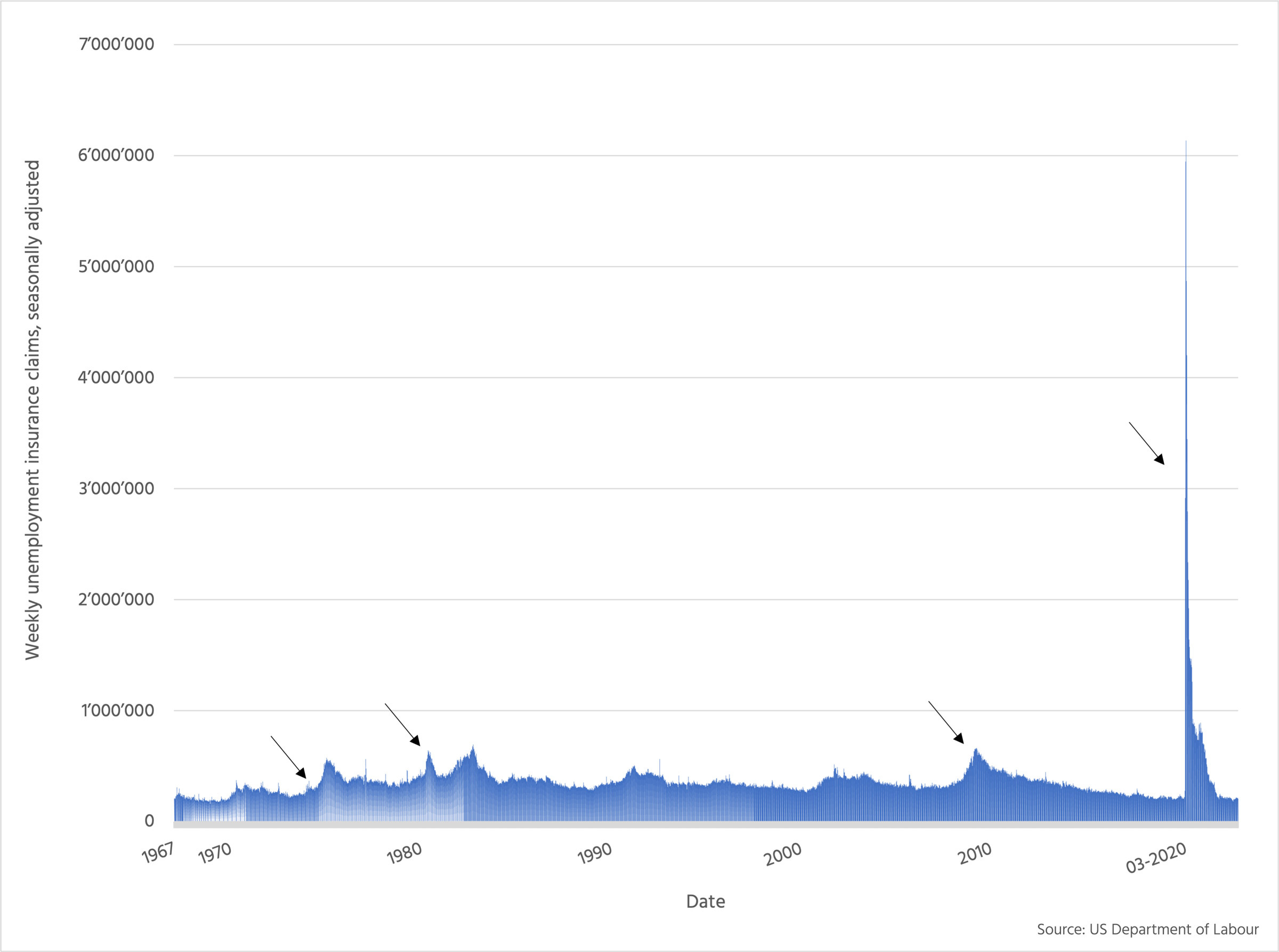

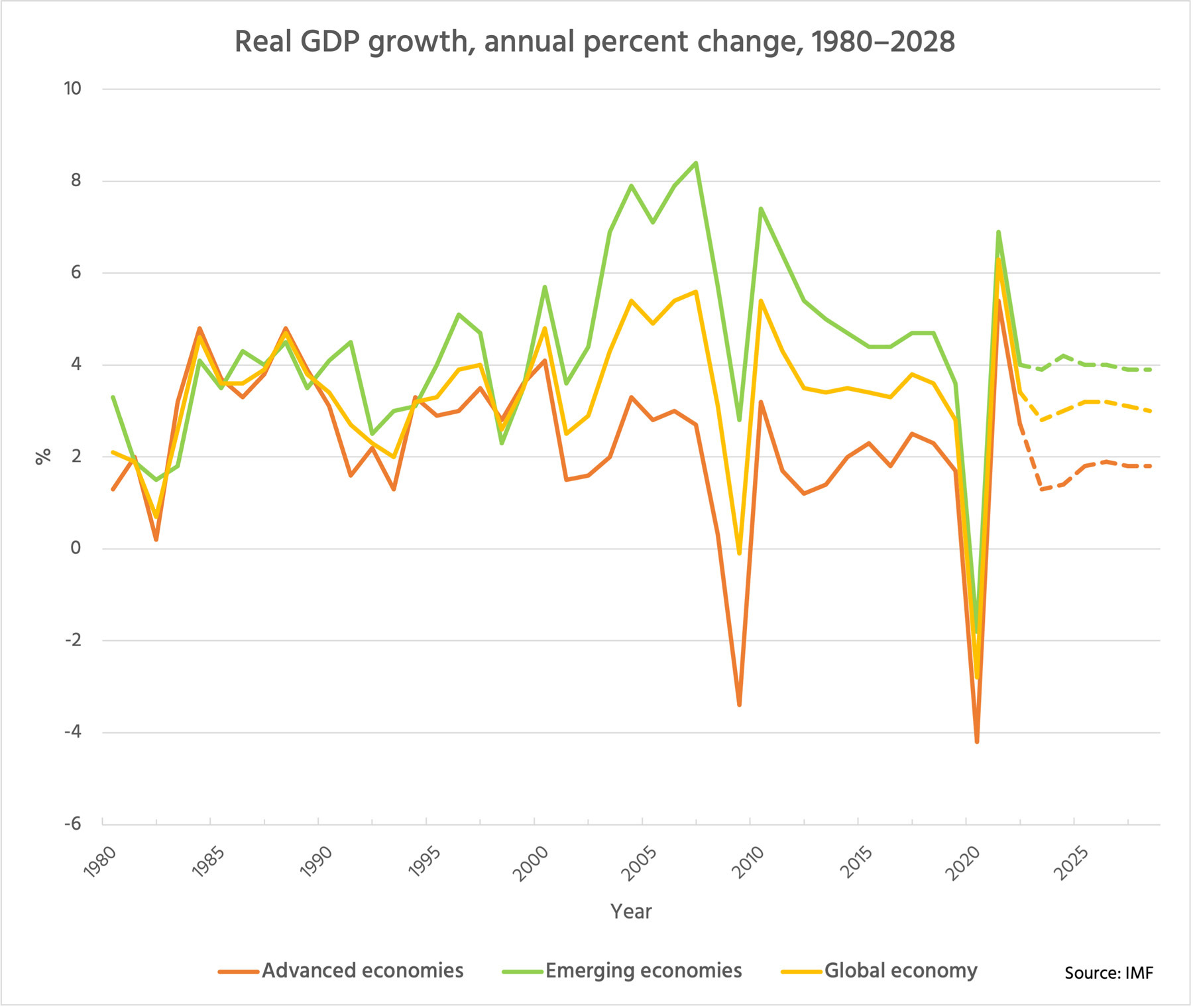

Recent economic indicators support The Lancet’s projections. US unemployment figures, which previously have tracked the pandemic as a whole – by showing an initial sharp, riving economic shock followed by a longer road to recovery, underpinned by US Federal and State government unemployment relief and the coordinated vaccine rollout nationwide – are continuing to do so, with weekly unemployment insurance claims returning to historic (pre-COVID-19) levels, indicating a welcome return to some level of normality. See Figure 3. Actual and real GDP growth shows a similar pattern, with severe disruption occasioned by the onset of the pandemic, a sharp recovery from 2021–2022 onwards, with projections indicating a return to near-historical levels of growth for 2023–2028. See Figure 4.

Figure 3. US weekly unemployment claims (seasonally adjusted), 1967–.

Figure 4. IMF actual and projected real GDP, annual percent change, 1980–2028, for global, advanced, and emerging economies.

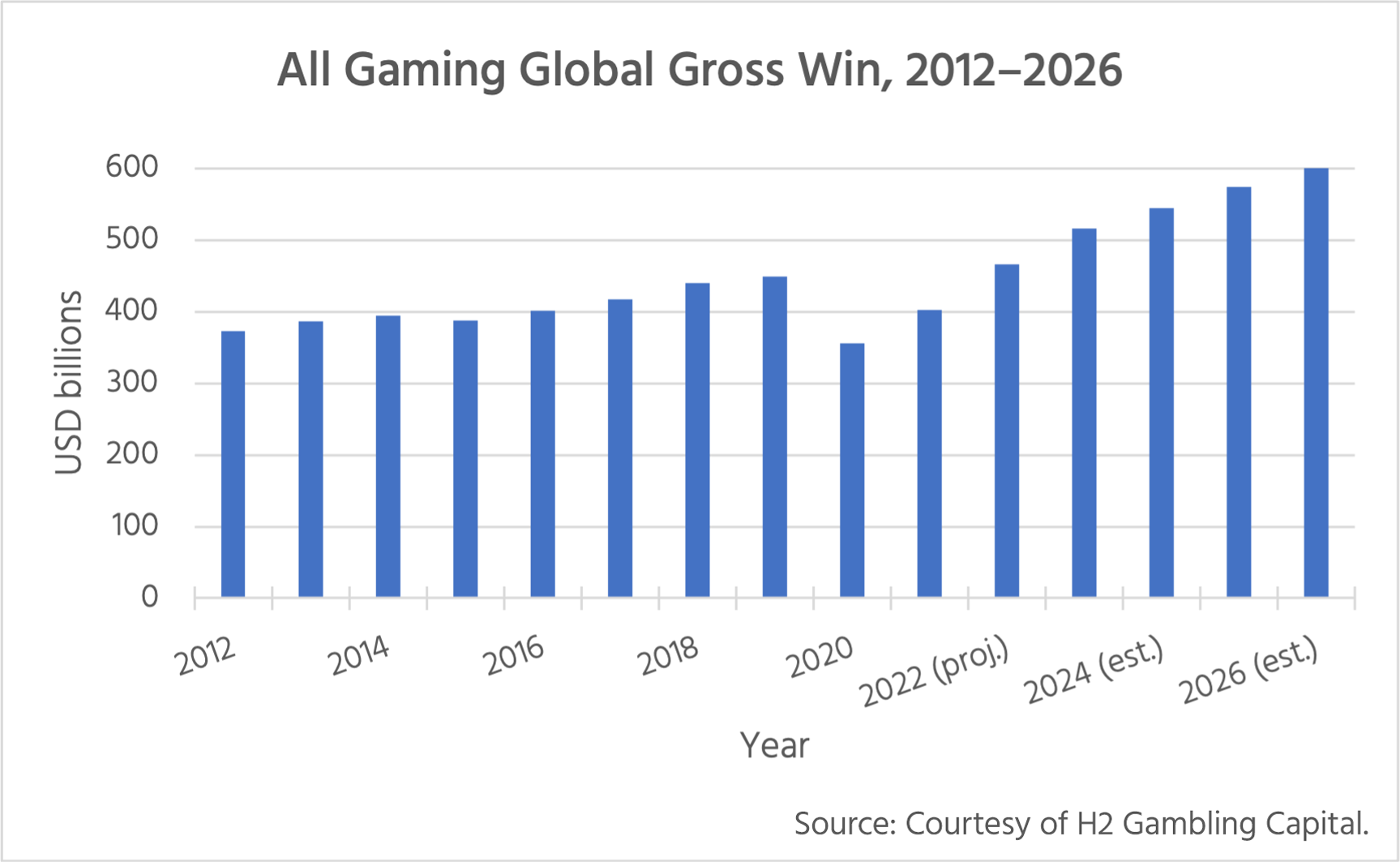

For lotteries and sports betting operators, the history of the pandemic has followed a similar arc to the general economy globally: an initial major dislocation and recovery through to end 2020, followed by a period of significantly increased spend – sometimes to record levels – through 2021 and 2022. Evidence is now beginning to emerge that the recovery of the lottery and sports betting sector is indeed ‘sticky’: sales for the lottery and sports betting sector are estimated to have returned to the levels seen pre-pandemic, and H2GC projects revenues will continue to rise for both lotteries and all gaming going forward. See Figure 5.

Turning to the future, the WLA will continue to report on developments in the lottery and sports betting sector, hopefully returning to more regular reporting as the disruption caused by the COVID-19 pandemic recedes. We look forward to bringing you the next edition in due course, and thank our audience for their attention during the COVID-19 pandemic.

Figure 5. H2GC actual and projected outlook, 2012–2026, for global gross win (lotteries) and global gross win (all gaming).

https://www.world-lotteries.org/insights/editorial/blog/lotteries-and-sports-betting-operators-emerge-largely-unscathed-from-pandemic