18

// PUBLIC GAMING INTERNATIONAL // May/June 2015

interact with other people and to make and touch things. Therefore,

retailers are responding to the new challenge through innovation, and

the most prominent ones are investing heavily in developing digital

marketing and ecommerce capabilities: 9 of the top 12 ecommerce

retailers are companies with established brick-and-mortar operations

(source: Global ecommerce Research, Internet Top 500 Retailers in

2013) who are reacting to the evolving context.

As a result, the line between brick-and-mortar and online operations

is blurring; more and more corporations are focusing on the

omnichannel experience they can provide to create new sources of

value. A few examples:

›

Established retailers are pushing hard to develop their digital

capabilities; Walmart now operates ecommerce websites in 10

countries; its largest, Walmart.com, sees 45 million visits a month,

a number that is growing every year.

›

More and more retailers are offering their physical stores as point

of delivery for goods purchased online; on the other end it is

rumored that Amazon is considering building physical stores.

›

Apple appointed Angela Ahrendts, the former CEO of

luxury brand Burberry, SVP for online and retail stores, clearly

recognizing the opportunity to managing the two channels as a

single integrated means to reach out to customers.

Mobile is part of this trend, and it is increasing its market shares

among online sales:

›

According to Criteo, in Q1 2015, 34% of all global ecommerce

transactions, and 29% in the U.S., were via mobile.

›

A senior executive at Walmart declared that over the 2014

Holiday season, mobile represented “70% of the orders … taken

through [their] digital business.”

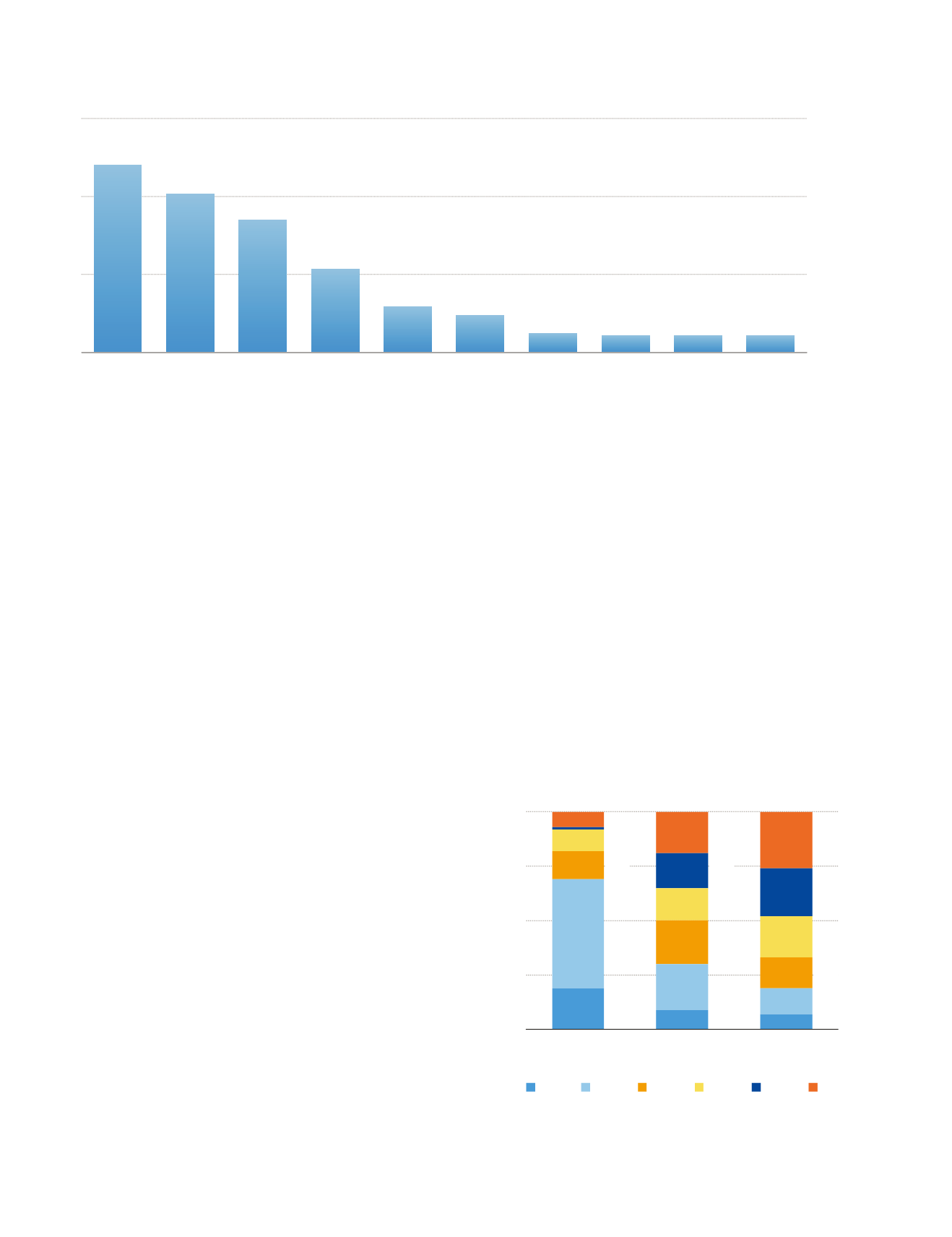

Lotteries are taking part in this transformation; since the 1990s, the

interactive channel has been a key international growth driver. Today

several European lotteries see more than 25% of their sales being

generated through digital channels (see Figure 1).

iLottery is also a key driver tomodernize the lottery brand and to enable

lotteries to be more relevant for consumers. The interactive channel:

›

Attracts the young adult demographic that traditionally has been

more difficult to serve effectively (see Figure 2 for an example

from a European jurisdiction of the demographics of different

games/channels).

›

Enables innovative content and innovative ways to promote, for

example through social spaces, traditional games.

These are all opportunities that need to be embraced by lotteries and

their most loyal evangelists, the retailers.

In lottery and the general retail industry, interactive does not

necessarily cannibalize retail sales, and can in fact be leveraged not

only to improve player convenience but also to make the retailers

a more attractive destination for consumers. The increased use

of personal devices and smartphones can accelerate in-store

innovations and improve the retail experience. New devices such as

digital mirrors, which take a 360-degree video, allowing clients to see

Age Distribution of Customer Base (percent)

0%

25%

50%

75%

100%

Internet Lottery

Retail Instant Tickets Retail Lotto Games

18-24

24-34

35-44

45-54

55-64

>64

7%

1%

10%

13%

50%

19%

19%

16%

20%

21%

9%

15%

26%

22%

14%

12%

7%

19%

Figure 2 – Player Demographics of Interactive Lottery vs. Retail Lottery

(example of a European lottery jurisdiction)

International Benchmark on Internet Sales Penetration over Total Lottery Sales (percent)

Finland

Denmark

Sweden

UK

Norway

New Zealand

Switzerland

Portugal

France

Luxembourg

3.6%

3.7%

3.7%

4.2%

7.9%

9.7%

17.9%

28.4%

34%

40.1%

Figure 1 – Top European Lotteries for Interactive Sales